NEW ROCHELLE, NY (June 9, 2026) — For the second consecutive year, a New Rochelle Finance Commissioner appeared before the City Council at a Committee of the Whole meeting alongside auditors from EFPR Group to present audit results without making the underlying financial report available to council members or the public — leaving no way to verify the figures presented or the answers given to council questions.

Last year, Finance Commissioner Edward Ritter presented preliminary audit results at a September 9, 2025 Committee of the Whole meeting but did not file the 2024 Year End Financial Report with the New York State Office of the State Comptroller until December 2025. Ritter retired and never returned to present the filed report to the council.

This year, Finance Commissioner Alistair Featherstone presented audit results at a June 9, 2026 Committee of the Whole meeting. The 2025 Year End Financial Report has not been filed with the State Comptroller. It has not been made available to the public. The dollar amount of an illegal $19 million fund transfer — a state law violation identified by auditors — did not appear in the slide deck at all. It emerged only when a council member asked.

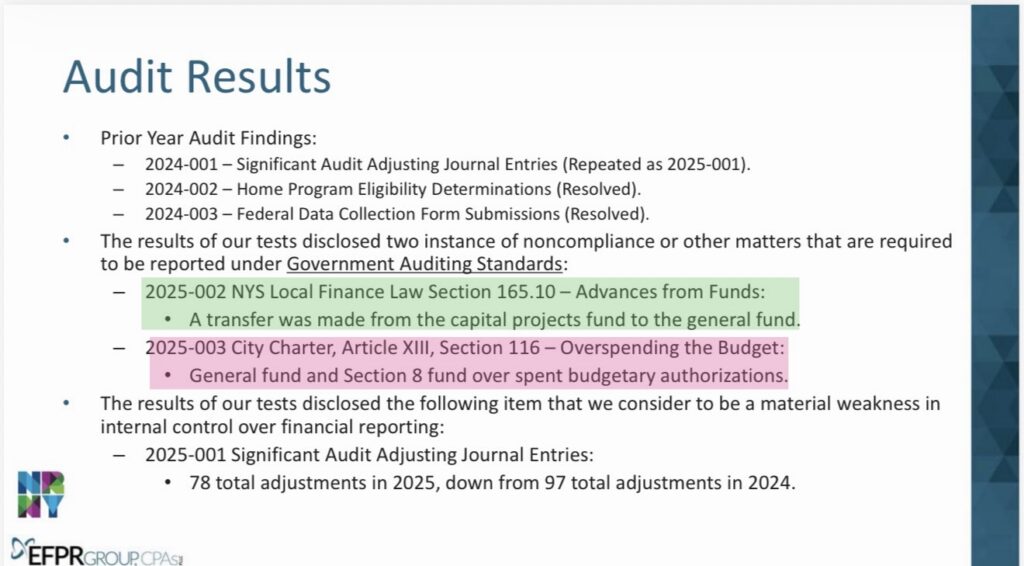

New Rochelle’s independent auditors have identified two violations of state law and repeated a finding of material weakness in internal controls in their review of the city’s finances for the year ending December 31, 2025, according to a presentation delivered to the City Council on Tuesday by EFPR Group CPAs.

The findings come against a backdrop of documented financial mismanagement under the Ramos-Herbert administration that Talk of the Sound has reported on extensively since 2025 — and they were delivered by the same auditing firm that withheld documents from the public at a September 2025 Committee of the Whole meeting, drew sharp complaints from council members about the practice, and is now doing it again.

An Illegal Fund Transfer

Auditors identified a transfer from the capital projects fund to the general fund that violated New York Local Finance Law Section 165.10 (in green, above), which governs advances between municipal funds. The transfer is listed as finding 2025-002.

The presentation does not disclose the dollar amount. Talk of the Sound has requested the full 2025 Year End Financial Report from the City Clerk’s office. If the city declines to provide it voluntarily, a FOIL request will follow.

New York Local Finance Law Section 165.10 is not ambiguous. It sets specific conditions under which advances between funds are permitted. A transfer that violates those conditions is not a bookkeeping error. It is a violation of state law. The question of who authorized the transfer — and whether the City Council approved it as required under the City Charter — has not been publicly answered.

UPDATE: Auditors identified a transfer from the capital projects fund to the general fund that violated New York Local Finance Law Section 165.10, which governs advances between municipal funds. The transfer is listed as finding 2025-002. The dollar amount did not appear anywhere in the EFPR slide deck — it emerged only because Council Member Shane Osinloye asked directly during the meeting. Finance Commissioner Alistair Featherstone answered: approximately $19 million. The explanation offered was that the city needed to cover school tax payments to the district before mortgage payment receipts arrived — a timing issue, in the administration’s framing. Featherstone confirmed the general fund owes that money back to the capital fund.

No council member followed up to ask who authorized the transfer, whether the City Council approved it as required under the City Charter, or whether the violation triggers any reporting obligation to a state oversight agency. Those questions remain unanswered.

Overspending the Budget

The second noncompliance finding (2025-003 in pink, above) involves the city overspending its budgetary authorizations in both the general fund and the Section 8 fund, in violation of City Charter Article XIII, Section 116.

Spending beyond appropriated amounts without council authorization is not a technicality. The City Charter exists precisely to prevent city officials from spending money the council has not approved. That both the general fund and the Section 8 fund exceeded their authorizations in the same year raises the question of whether this reflects a pattern of disregard for the fiscal controls the Charter imposes.

A Repeated Material Weakness

For the second consecutive year, auditors flagged a material weakness in internal controls over financial reporting, stemming from the volume of audit adjusting journal entries required to correct the city’s own bookkeeping. The number fell from 97 adjustments in 2024 to 78 in 2025 — a modest improvement, but the finding itself was carried forward unchanged as finding 2025-001.

A material weakness is the most serious category of internal control deficiency an auditor can identify. It means there is a reasonable possibility that a material misstatement of the city’s financial statements would not be prevented or detected on a timely basis by city staff. The city has now failed to remediate this finding for at least two consecutive years.

This is the same Brian Sawma of EFPR Group who appeared before the City Council in September 2025 and spent more than an hour presenting an incomplete preliminary audit while helping then-Finance Commissioner Edward Ritter conceal a $4.5 million error — a fact Ritter did not disclose until pressed repeatedly by Council Member Shane Osinloye. At that same meeting, Osinloye and other council members demanded that audit materials be provided in advance. Nothing changed. Tuesday’s session was a repeat of the same pattern: documents withheld, council and public left to absorb financial findings in real time, with no opportunity for meaningful review beforehand.

The Fund Balance: Context Required

The unassigned General Fund balance rose sharply in 2025, from $10.5 million at the end of 2024 to $23.1 million — an increase of $12.6 million in a single year. Property tax collections drove much of the gain, rising $8.7 million to $75.3 million. Sales tax collections also grew, adding $1.5 million.

That number requires context.

As Talk of the Sound reported in September 2025, the Ramos-Herbert administration had by that point burned through more than $15 million in unassigned fund balance in roughly 18 months — a decline of more than 63% from the $24.5 million the city carried when the current administration took office on January 1, 2024. The depletion was not accidental. Fund balance was drawn down to cover a pattern of spending that included $384,825 on events and celebrations in 2024 alone, politically connected program funding, and overtime costs — much of it authorized through a series of mid-year legislative actions that individually appeared modest but collectively drained reserves at an unsustainable rate.

Sources with direct knowledge of the year-end closing process told this publication that auditors were forced to unwind transactions that had been moved between line items and backfilled from the fund balance, and that the administration had anticipated that development revenues — including approximately $12-13 million owed by Twining Properties in connection with the Pratt Landing project — would replenish reserves before auditors arrived. That money never materialized. It still has not been paid.

The 2025 rebound reflects in part a correction from an artificially depressed baseline, in part strong tax collections, and in part the city’s stated decision — for the first time in three years — to adopt a budget that appropriated no unassigned fund balance. It is not evidence of sound financial management. It is evidence that the bleeding has, for now, slowed.

Meanwhile, the city’s overall financial position remains deeply negative. As of December 31, 2024 — the most recent year for which a complete audited financial report is available — New Rochelle’s total net position stood at a deficit of $179.1 million, a figure that declined year over year. The 2025 full report has not yet been made public.

New Finance Commissioner, Same Unanswered Questions

Edward Ritter, who served as Finance Commissioner during the period of the fund balance collapse and whose September 2025 presentation to the City Council was marked by incomplete disclosures and at least one concealed error, retired on December 1, 2025. His successor, Alistair Featherstone, was appointed in January 2026. Featherstone brings more than 20 years of municipal finance experience, including public finance investment banking at Oppenheimer, Bank of America, and CastleOak Securities.

Whether Featherstone can stabilize a finance operation that has produced two consecutive years of material weakness findings, two new state law violations, and a fund balance that was deliberately depleted and then partially rebuilt remains to be seen. The structural problems — an administration that spent money it did not have, a city manager who signed off on it, and a council that was kept in the dark — did not retire with Ed Ritter.

What the Annual Report Would Tell Us — If It Existed

Underlying all of this is a more fundamental problem. The Annual Comprehensive Financial Report for the year ending December 31, 2025 has not been made public. What was presented to the City Council on Tuesday was a slide deck — a summary prepared for a public audience, not the audited financial report itself. The full report contains the complete findings, the management letter, the dollar amounts associated with each violation, and the detailed narrative on every deficiency. Until that document is released, it is not possible to fully assess the magnitude of what the auditors found. New Rochelle presented a preliminary audit to the public in September 2025 before the 2024 report was finalized — and the 2024 report, when it finally emerged, told a significantly worse story than the presentation suggested. There is no reason to assume the pattern will not repeat itself.

The dollar amount of the illegal fund transfer has not been disclosed. The identity of the officials who authorized it has not been disclosed. The mechanism by which both the general fund and Section 8 fund exceeded their budgetary authorizations has not been explained. And the Twining Properties balance — roughly $13 million owed to the city in connection with Pratt Landing — remains unpaid, with no public accounting of when or whether it will be collected.

Those questions remain open. This publication will continue to report on them

RELATED

New Rochelle Touted Strong Finances as Fund Balance Collapsed Before Audit Was Finalized (3/18/2026) Finance & Auditor presentation last fall highlighted a “clean audit,” but the 2024 financial report shows a $179 million deficit, sharply reduced reserves and significant audit adjustments.

Butcher’s Bill Comes Due for New Rochelle Democrats (Sept. 7, 2025) Analysis of financial decisions and policies contributing to mounting fiscal pressures

New Rochelle Fund Balance Q&A Devolves Into Unintelligible Mush (Sept. 10, 2025) City officials struggle to explain declining fund balance during a contentious public discussion

Hidden Audit Presentation Records Released by New Rochelle (Sept. 11, 2015) Previously undisclosed audit presentation materials reveal internal concerns and financial reporting issue.

New Rochelle Annual Comprehensive Financial Report December 31, 2024 (Nov. 5, 2025) Official financial report showing a $179 million negative net position, sharply reduced reserves and audit-related adjustments.

This article was prepared with the assistance of AI tools under the direction and editing of Robert Cox.

Have information about this story? Email robertcox@talkofthesound.com (preferred) or contact via WhatsApp: +353 089 972 0669.